In addition to not issuing dividends and not being included in EPS calculations, treasury shares also have no voting rights. The amount of treasury stock repurchased by a company may be limited by its nation’s regulatory body. In the United States, the Securities and Exchange Commission (SEC) governs buybacks.

How do I record Treasury Stock using the par value accounting method?

Upon reissuance, any amount received in excess of the carrying amount of the treasury shares must be credited to the Capital Stock account. This is because no other paid-in capital account exists for no-par-value stock. When the shares are reissued, Cash is debited for the proceeds and Treasury Stock is credited for the par value of charitable contributions 2020 the shares. Any additional credit is recorded in Capital in Excess of Par, just as if the stock is being issued for the first time. At the time of acquisition, the Treasury Stock account is debited for the par value of the shares, and Capital in Excess of Par is debited for the original amount paid in excess of par at issuance.

- Treasury stock is the corporation’s own capital stock, either common or preferred, that has been issued and subsequently reacquired by the firm, but not canceled.

- This arrangement permits the corporation to retire the shares and avoid future dividend payments.

- The following discussion focuses on the most straightforward types of transactions.

- The difference between the actual price paid and the par or stated value of treasury shares is recorded in an account known as gain or loss on purchase and sale of stock.

AccountingTools

Additional shares obtained through the treasury stock method factor into the calculation of the diluted earnings per share (EPS). This method assumes that the proceeds a company receives from an in-the-money option exercise are used towards repurchasing common shares in the market. Notice on the partial balance sheet that the number of common shares outstanding changes when treasury stock transactions occur. The 800 repurchased shares are no longer outstanding, reducing the total outstanding to 9,200 shares. When shares are repurchased, the treasury stock account is debited to decrease total shareholders’ equity.

Q. Why do companies buy back their own stock?

If a company purchases treasury shares and then does not re-sell them, there would be no effect on either assets or Retained Earnings. Treasury Stock is the corporation’s own capital stock, either common or preferred, that has been issued and subsequently reacquired by the firm, but not canceled. Thus, one way the corporation can avoid dividend restrictions is to purchase treasury stock. As a result, when creditors require restrictions on dividend payments, they also often require restrictions on treasury stock purchases. Finally, no treasury stock held by the corporation has any dividend or voting rights.

The cash account is credited for the amount paid to purchase the treasury stock. Treasury shares are not considered as outstanding stock because they do not receive dividends and cannot effectively vote at meetings. They belong to the issuer even when they were initially issued at a discount rather than the market price. They can be in the form of both common and preferred shares, depending on whether investors prefer risk or reward. These shares do not receive dividends and cannot effectively vote at meetings.

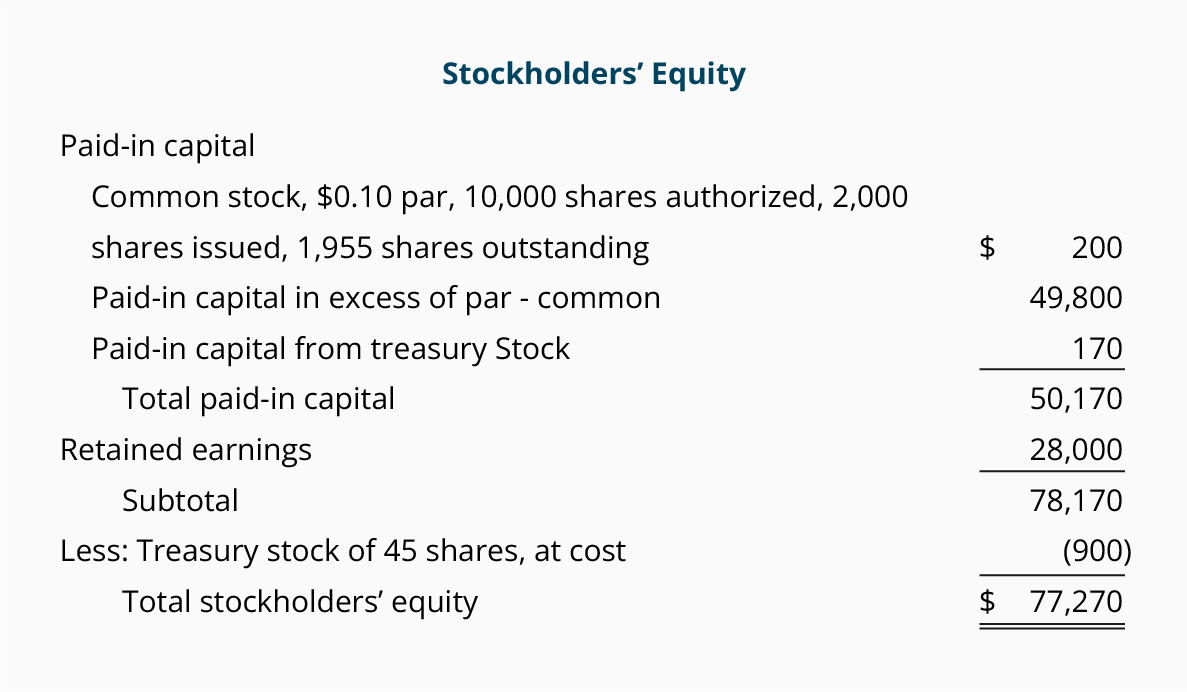

The common stock account reflects the par value of the shares, while the APIC account shows the excess value received over the par value. Treasury stock is a contra equity account recorded in the shareholders’ equity section of the balance sheet. Because treasury stock represents the number of shares repurchased from the open market, it reduces shareholders’ equity by the amount paid for the stock. Even though the company is purchasing stock, there is no asset recognized for the purchase. Immediately after the purchase, the equity section of the balance sheet (Figure 5.62) will show the total cost of the treasury shares as a deduction from total stockholders’ equity.

If the proceeds are less than the original cost, Additional Paid-In Capital should be debited. For no-par stock with a stated value, the entries for the purchase and sale of treasury shares are the same as those described above. Under the par value method, the Treasury Stock account should be viewed as contra to the Capital Stock account.

Second, securities laws restrict the amount of purchases and sales by the board due to the potential for manipulation, as well as their access to insider information not available to the public. Such stock, which is held in the corporate treasury, loses its right to vote, receive dividends, or receive assets upon liquidation. In comparison to our starting point, the basic EPS of $2.00, and the diluted EPS is $0.10 less. Each tranche has a strike price, which the option holder must pay to exercise the option as part of the contractual agreement.

Another reason for acquiring treasury stock exists for corporations whose shares are not traded on an active basis. In these cases, the board may accommodate stockholders by agreeing to buy their shares when they wish to liquidate their holdings. Treasury stock is the corporation’s own capital stock, either common or preferred, that has been issued and subsequently reacquired by the firm, but not canceled. We can then subtract the 5,000 shares repurchased from the 10,000 new securities created to arrive at 5,000 shares as the net dilution (i.e., the number of new shares post-repurchase). If we were calculating the basic EPS, which excludes the impact of dilutive securities, the EPS would be $2.00. Besides options, other examples of dilutive securities include warrants and restricted stock units (RSUs).

By increasing the value of the shareholders’ interest in the company (and voting rights), the repurchase of shares helps fend off hostile takeover attempts. If the shares are priced correctly, the repurchase should not have a material impact on the share price – the actual share price impact comes down to how the market perceives the repurchase itself. If the company’s share price has fallen in recent periods and management proceeds with a buyback, doing so can send out a positive signal to the market that the shares are potentially undervalued. Therefore, an increase in treasury stock via a share buyback program or a one-time buyback can cause the share price of a company to “artificially” increase.